Alternative data

This interesting article on quant traders' use of alternative data caught my attention in the last month. The author Justina Lee has recently done amazing journalistic work on the world of quantitative trading and investing for Bloomberg. She shows how "the decade-long boom in alternative data is reaching fever pitch on Wall Street." However, deriving trading insights from alternative data ranging from traffic-congestion statistics to job listings and credit card data is not easy at all.

She gives the example of how a trader from a Boston-based quant firm (PanaGora) found that those stocks recommended on the Seeking Alpha blog would increase in price for five days. The trader used this ‘signal’ to build a trading algorithm that was successful for some time, but then stopped working altogether after 2 years. The trader asks two important questions about the use of alternative data: first, was the strategy a fluke or was it real? Second, will the strategy keep working after everybody uses it? (basically human actions that might lead to market performativity are often not profitable!)

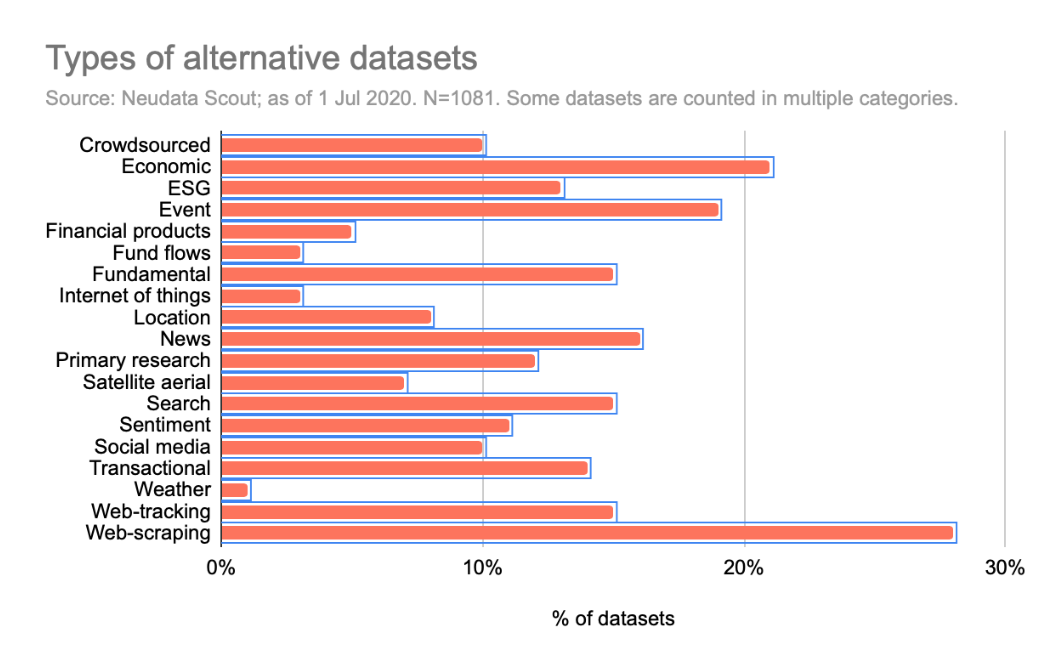

This is a warning for those traders who intend to use packaged sets of alternative data that have supposedly been backtested. Neudata—an IT service management company specialized in alternative data consulting—estimates that the financial industry's spending on alternative data surged to $1.7 billion in the last 5 years. The screenshot below shows the most used alternative data according to Neudata’s web site.

Compare also the industry figures provided by AlternativeData.

A few years ago I read this FT article by Robin Wigglesworth (I’m a big fan of his work too) about the fact that "there are more than 1bn websites with more than 10tn individual web pages, with 500 exabytes of data." Roughly, imagine that only 1 exabyte could store more than 300 billion of MP3 songs.

Basically this is a data deluge that begs the questions: can investment managers and traders really process and use alternative data effectively? A question close to the issue dealt by Armin Beverungen and Ann-Christina Lange in their paper on cognition and high-frequency trading. Read it ‘cause they build on Katherine Hayles’s book Unthought!

Alternative data is such an interesting research area for social scientists. I found this recent book on alternative data by Denev and Amen very useful to understand the universe of alternative data and how institutional investors use them to get an edge.

Mom-and-pop traders

Another interesting story in the news was how retail investment platforms such as Robinhood enabled small investors to push the ‘buy-the-dip mentality’ to the extreme, buying insolvency stocks such as Hertz Global Holdings Inc. To many, that’s a bad sign of investment mania. Almost 40,000 Robinhood users bought the Tesla stock in four hours on 13 July 2020. No need to comment the Tesla Inc. share price graph below…

Of course, the first book that came up in my mind is McKay's Extraordinary popular delusions and the madness of crowds (1841) as an early study of crowd psychology. History repeats itself.

Wirecard

Let's conclude with the Wirecard story. The Financial Times made amazing investigative journalism on Wirecard and helped expose Wirecard’s wrongdoings. Kudos to Dan McCrum and colleagues!

I always thought one must not be a genius to realize that Wirecard was a dodgy company. I mean... Wirecard initially specialized on providing payment services to porn and online gambling web sites. Then it went on a massive M&A spree and jumped on the post-2008 fintech bandwagon (AI and machine learning) to become one of the largest companies quoted on the Frankfurt Stock Exchange. They call it the new Enron story. It reminds me more of Parmalat faking fictitious money in a Bank of America account at the Cayman Islands.

Anyway, the story of Wirecard will finally bring a reality check to the fintech sector. According to this FT article, the fintech sector in general should expect greater regulatory scrutiny “due to its rapid growth and use of multiple third-party service providers.”